Key Takeaways:

- AI remained the dominant investment theme globally.

- Technology and semiconductor stocks drove most equity market gains.

- Asian markets significantly outperformed, led by South Korea and Japan.

- Inflation stayed elevated but did not derail risk appetite.

- Gold and oil weakened despite geopolitical uncertainty.

- Silver benefited from both industrial and precious-metal demand.

- The U.S. dollar remained relatively stable.

- Investor optimism surrounding AI valuations, SpaceX’s IPO plans, and trillion-dollar technology companies continued to fuel market momentum.

U.S. Stock Indices Close at New Record Highs

U.S. equities delivered another impressive performance in May 2026, with all major indices finishing the month in positive territory as investors continued to embrace artificial intelligence-related opportunities despite persistent inflation and geopolitical uncertainty. The Dow Jones Industrial Average rose from 49,714 to 51,010, gaining 2.61% during the month. The broader S&P 500 climbed from 7,206 to 7,577, recording a gain of 5.15%, while the technology-heavy Nasdaq 100 outperformed significantly, surging 10.57% from 27,427 to 30,326. Small-cap stocks also participated in the rally, with the Russell 2000 advancing 3.99% from 2,804 to 2,916.

The primary driver behind the strong performance remained the artificial intelligence sector. Investor optimism intensified after Anthropic’s latest funding round reportedly pushed the company’s valuation close to the $1 trillion mark, highlighting the enormous amount of capital still flowing into AI infrastructure and large language models. The AI boom also continued to benefit semiconductor companies, with Micron reaching a $1 trillion valuation milestone as demand for memory chips and AI-related hardware accelerated. Adding to investor excitement, SpaceX announced plans for an initial public offering, further reinforcing confidence in high-growth technology and innovation-focused sectors.

Economic data remained mixed throughout the month. The latest inflation figures showed headline PCE inflation at 3.8%, while Core PCE came in at 3.2%. Although both readings remained above the Federal Reserve’s target, markets largely viewed the data as manageable and continued to focus on the possibility of policy easing later in the year. As a result, investors remained willing to pay premium valuations for growth-oriented assets, particularly within the technology sector.

Asian Stocks Outperform Global Markets

Asian equity markets significantly outperformed many of their global counterparts in May, driven by strong semiconductor demand and continued enthusiasm surrounding artificial intelligence. Japan’s Nikkei index rose from 59,379 to 66,329, delivering an impressive monthly gain of 11.70%. The rally was supported by strong corporate earnings, continued foreign investment inflows, and robust performance from export-oriented technology companies benefiting from global AI demand.

South Korea’s Kospi was among the strongest-performing major indices globally, surging from 6,782 to 8,476 and recording an extraordinary gain of 24.98%. Much of the strength came from the semiconductor sector, where investors continued to increase exposure to companies expected to benefit from the AI infrastructure boom. Both Samsung Electronics and SK Hynix reached the symbolic $1 trillion valuation milestone during the month, reflecting strong expectations for future earnings growth as demand for high-bandwidth memory chips and advanced semiconductors continues to accelerate. The combination of strong earnings, government support for technology industries, and increasing foreign capital inflows helped Asian markets outperform most developed markets during May.

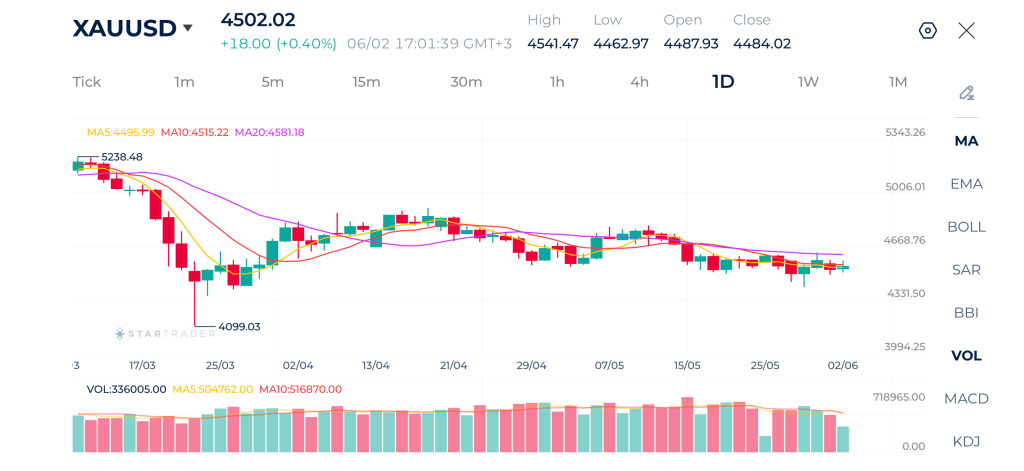

Commodities Remain Volatile as Geopolitical Tensions Weigh on Sentiment

Commodity markets experienced heightened volatility throughout May as investors weighed geopolitical risks against concerns about future economic growth. Gold began the month at $4,625 per ounce but finished lower at $4,520, representing a decline of 2.27%. Normally, ongoing geopolitical tensions and military conflicts would support safe-haven demand for gold. However, the strong rally in equity markets, particularly within technology stocks, encouraged investors to rotate capital toward risk assets, limiting demand for the precious metal despite elevated global uncertainty.

Silver, on the other hand, managed to post gains during the month. The metal rose from $73.25 to $75.20 per ounce, increasing 2.66%. Unlike gold, silver benefits not only from its role as a precious metal but also from its extensive industrial applications. Growing demand from AI infrastructure, data centers, advanced electronics, and renewable energy projects continued to support silver prices, allowing it to outperform gold.

Oil markets experienced the largest decline among major commodities. Brent crude fell sharply from $109.80 per barrel at the beginning of May to $91.45 by month-end, a drop of 16.71%. While geopolitical tensions initially supported oil prices, concerns about slowing global economic growth and expectations that supply disruptions would remain contained ultimately weighed on the market. Ongoing uncertainty surrounding negotiations involving Iran and developments in the Middle East also created significant volatility, causing oil prices to react sharply to changing headlines throughout the month.

The US Dollar Achieved Modest Gains

The U.S. dollar remained relatively stable during May. The U.S. Dollar Index (DXY) started the month at 98.12 and ended at 98.42, recording a modest gain of 0.31%. The limited movement reflects the balance between competing market forces. On one hand, inflation remained elevated, supporting expectations that the Federal Reserve would maintain a relatively restrictive policy stance. On the other hand, improving risk sentiment and strong equity market performance reduced demand for traditional safe-haven assets, including the dollar.

Overall, May 2026 was characterized by a continued dominance of the artificial intelligence investment theme, which overshadowed concerns about inflation, geopolitical risks, and slowing global growth. Technology stocks led gains across both U.S. and Asian markets, while trillion-dollar valuations became increasingly common among leading AI and semiconductor companies. Despite elevated inflation and ongoing geopolitical tensions, investors remained focused on long-term growth opportunities, helping global equity markets extend their historic rally and reinforcing the view that AI remains the defining investment narrative of 2026.

Outlook for June 2026

As markets enter June, investors are likely to face a more challenging environment after the exceptional gains recorded in May. While the artificial intelligence theme continues to provide strong support for equities, valuations across many technology and semiconductor companies have reached historically elevated levels, increasing the likelihood of periods of profit-taking and higher volatility.

In the United States, the primary focus will remain on inflation and Federal Reserve policy. Although markets have largely ignored elevated inflation readings in recent months, any upside surprise in upcoming CPI, PPI, or PCE data could challenge expectations for future rate cuts and create pressure on high-growth technology stocks. Investors will also closely monitor labor market data and consumer spending figures to assess whether the U.S. economy can maintain its resilience without reigniting inflationary pressures.

Asian markets could continue outperforming if demand for AI-related hardware remains strong. South Korea’s semiconductor giants, Samsung Electronics and SK Hynix, remain key beneficiaries of global AI infrastructure spending. Meanwhile, Japanese equities may continue to attract international investors due to strong corporate earnings, favorable corporate governance reforms, and continued demand for technology exports. Nevertheless, after May’s exceptional rally, both the Nikkei and Kospi could experience short-term consolidation before attempting further gains.

Commodity markets are expected to remain heavily influenced by geopolitical developments. Continued strength in stock markets could limit upside potential for traditional safe-haven assets. Silver may continue to outperform gold as industrial demand from the AI, electronics, and renewable energy sectors remains robust.

Oil prices are likely to remain highly volatile throughout June. Developments surrounding Iran, shipping routes in the Middle East, OPEC+ production policies, and global growth expectations will continue to drive market sentiment. While geopolitical tensions could create temporary price spikes, concerns about global economic growth may prevent a sustained recovery unless significant supply disruptions emerge.

In the foreign exchange market, the U.S. dollar could experience increased volatility as investors reassess the outlook for Federal Reserve policy. If inflation remains stubbornly high, the dollar may strengthen as markets push back expectations for rate cuts. Conversely, signs of cooling inflation could weaken the dollar and provide additional support for equities, commodities, and emerging market currencies.

Risk Disclaimer: This material is provided for informational purposes only and does not constitute a recommendation or investment advice. Trading financial instruments on margin involves substantial risk and may not be appropriate for all investors.

Tags

Open Live Account

Please enter a valid country

No results found

No results found

Please enter a valid email

Please enter a valid verification code

1. 8-16 characters + numbers (0-9) 2. blend of letters (A-Z, a-z) 3. special characters (e.g, !a#S%^&)

Please enter the correct format

Please tick the checkbox to proceed

Please tick the checkbox to proceed

Important Notice

STARTRADER does not accept any applications from Australian residents.

To comply with regulatory requirements, clicking the button will redirect you to the STARTRADER website operated by STARTRADER PRIME GLOBAL PTY LTD (ABN 65 156 005 668), an authorized Australian Financial Services Licence holder (AFSL no. 421210) regulated by the Australian Securities and Investments Commission.

CONTINUEImportant Notice for Residents of the United Arab Emirates

In alignment with local regulatory requirements, individuals residing in the United Arab Emirates are requested to proceed via our dedicated regional platform at startrader.ae, which is operated by STARTRADER Global Financial Consultation & Financial Analysis L.L.C.. This entity is licensed by the UAE Capital Market Authority (CMA) under License No. 20200000241, and is authorised to introduce financial services and promote financial products in the UAE.

Please click the "Continue" button below to be redirected.

CONTINUEError! Please try again.